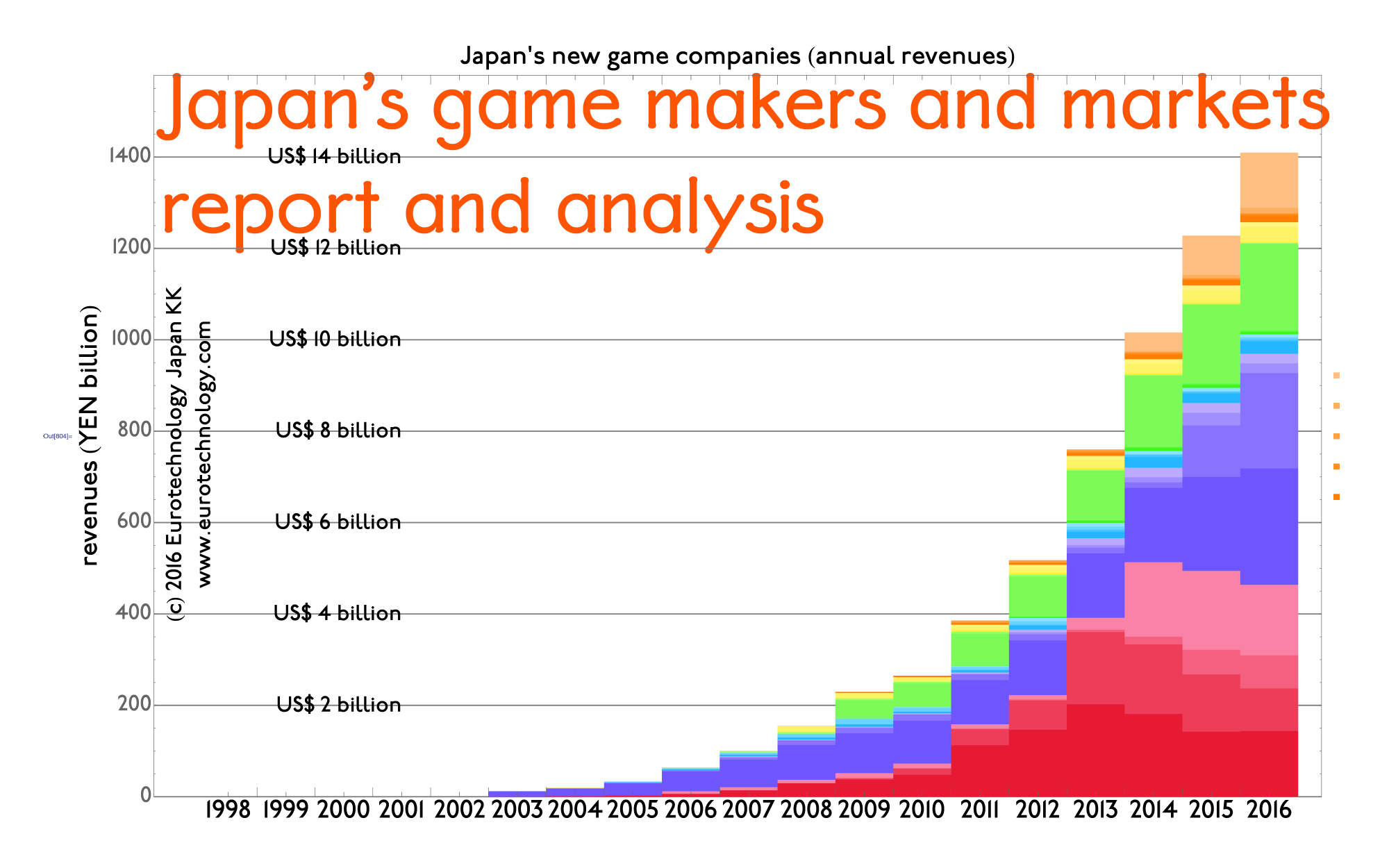

Google play apps Japan ranking in Japan by gross revenues

AppAnnie showed that in terms of combined iOS AppStore + Google play apps Japan revenues, Japan is No. 1 globally, spending more than the USA. Therefore Japan is naturally the No. 1 target globally for many mobile game companies!

AppAnnie showed that in terms of combined iOS AppStore + Google Play revenues, Japan is No. 1 globally, spending more than the USA. Therefore Japan is naturally the No. 1 target globally for many mobile game companies, and quite a few of the top grossing apps in Japan are of foreign origin – can you guess which?!

iOS AppStore-Japan “Top Grossing” ranking of February 10, 2015:

Fidelity: Japan market entry the patient and careful way

Fidelity’s Colt to acquire KVH for YEN 18.595 billion (€ 130.3 million = US$ 160 million)

Both Colt and KVH were founded with investments by Fidelity Investments and associated companies, Colt in London in 1992, and KVH in 1999 in Tokyo, as telecommunications service providers for the financial industry and other industrial customers. While KVH remained 100% owned by Fidelity and associated companies, Colt was listed on the London Stock Exchange in 1996.

Initially founded as telecommunications companies, both Colt and KVH have developed into “information delivery platforms” based on networking infrastructure, data centers, optical fibre networks and associated management and information services.

On November 12, 2014, Colt announced the plan to acquire KVH for YEN 18.595 billion (€ 130.3 million = US$ 160 million) in cash from KVH’s owner Fidelity Investments.

Since KVH is 100% owned by Fidelity Investments, and Colt have also been founded by Fidelity which is still a shareholder, the acquisition needs to be approved by independent Directors and by independent shareholders of Colt.

A General Meeting of Colt’s shareholder has been announced for December 16, 2014 at 10:00am in Luxembourg where the approval of shareholders of Colt will be sought.

Colt – the “information delivery platform”

Colt was founded by James P Hynes (Jim Hynes) with investments from Fidelity Investments and related companies in 1992 in London, and went public with an IPO on London Stock Exchange in 1996.

Colt operates 20 data centers and substantial optical fiber networks, and has more than 5000 employees.

Colt’s annual revenues are € 1,575.8 million (= US$ 2 billion) in 2013.

Colt market capitalization currently is UKL 1.19 billion (= US$ 1.9 billion).

KVH – “Asia’s information delivery platform”

KVH was founded by Fidelity Investments and related companies on April 2, 1999 in Tokyo.

KVH operates 9 Data Centers, owns optical fiber networks in Japan and to major financial centers in the world, and has about 590 employees.

KVH annual revenues are approx. € 133.6 million (= US$ 170 million) in FY2013, i.e. Colt is about 10 times bigger in terms of market cap and sales than KVH.

KVH owns optical fibre, ethernet, data center data infrastructure in Tokyo, Osaka and other parts of Asia. This photograph shows KVH owned cable infrastructure in the center of Tokyo

The planned acquisition values KVH at YEN 18.595 billion (€ 130.3 million = US$ 160 million), i.e. COLT is about 12 times bigger than KVH in terms of market capitalization/value.

Implications of acquisition of KVH by Colt – view as a Japan (and Asia) market entry by Colt

From the point of view of Colt, the acquisition of KVH – which has always been a sister company via the common investor Fidelity Investments, and common founder Jim Hynes – is a relatively low risk market entry into Japan and several other major Asian markets, and promises to have a very high chance of success for all parties.

We need to keep in mind, that essentially all other large scale market entries into Japan by infrastructure based telecommunication operators have failed: Vodafone, Cable & Wireless, WorldCom’s market entries into Japan’s telecom markets have all failed, and to our knowledge KVH is the only remaining internationally owned telecom infrastructure company in Japan today.

Essentially, both Vodafone and Cable & Wireless failed in Japan’s telecom markets, because they did not have the multitude of skills and know-how needed to manage a telecommunications business in Japan in a competitive manner. Colt with the acquisition of KVH acquires this know-how, and KVH at the same time has been an internationally managed company from the outset, so that Colt avoids the risks of acquiring a 100% Japanese companies such as Vodafone had done by acquiring Japan Telecom, with all the cultural issues that this entails.

At the same time, we also need to keep the scale in mind. While KVH has a market capitalization (i.e. the purchase price) of US$ 160 million, it can be argued that Vodafone-Japan could be expected to have a capitalization of around US$ 60 billion today had it been successful – i.e. about 375 times larger than KVH.

Japan’s largest telecommunication operator NTT currently has a market capitalization of US$ 62 billion, i.e. about 390 times larger than KVH, while SoftBank’s market capitalization is about 500 times larger than KVH’s.

Thus, if we see Colt’s acquisition of KVH as a market entry into Japan by a European telecom operator, then this is on an approx. 300-400 times smaller scale than Vodafone’s failed market entry into Japan, and with far better circumstances, and a far higher chance of success, and in our view with very carefully controlled risks.

Without doubt, a merger of KVH with Colt was on the minds of Fidelity Investments and Jim Hynes, when they founded both KVH and Colt in the 1990s.

What can we learn from Vodafone’s failure in Japan?

by Gerhard Fasol

Had Vodafone been successful in Japan, Vodafone’s Japan business could be worth € 40 billion (US$ 50 billion) today

In a separate blog post “EU-Japan Management: What is the value of good management?” we analyze what the value of Vodafone’s Japan business might be today, had Vodafone succeeded in Japan, based on current market values of the comparable companies NTT-Docomo, KDDI and Softbank, and we conclude that it is not unreasonable to assume that Vodafone’s Japan business could be worth € 40 billion (US$ 50 billion) today, had it been successful.

Vodafone Japan? Why did it fail and sell to SoftBank? – Quick answer

Vodafone Japan failed not for one single reason but for hundreds of reasons, which can be grouped into soft factors (mainly lack of understanding Japan and Japan’s telecom markets and it’s true size) and hard factors (mainly far too low investment) – read more details in our SoftBank-report:

Soft factors:

Japan knowledge at HQ, and knowledge at HQ about the specifics of Japan’s telecom sector (or lack thereof).

choice of management structure (there were attempts to correct the management structure, however too little and too late).

attitude displayed both privately e.g. within the Japanese industry sector and publicly via marketing messages and advertising

choice of executives and lower ranking managers and their knowledge and experience in Japan’s telecom sector (or lack thereof)

lack of sufficient know-how and experience to manage a large Japanese company, and particular the chain of retail stores

lack of management and execution know-how in Japan: tried three (3!!) times to introduce / roll-out 3G services in Japan, and failed every time to attract sufficient subscribers. As a result Vodafone Japan was far behind in 3G introduction. Only after sale to SoftBank, did SoftBank succeed in implementing the transition to 3G

too high expectations for profitability and margins from HQ, which were out of line with profitability and returns usual in Japan, and out of line of competitor’s margins

and many more

Hard factors:

far too low budgets for infrastructure investment resulting in much lower coverage and network quality compared to competitors NTT-DoCoMo and KDDI/au and TuKa, Willcom and others. As a consequence of far too low investment budgets, Vodafone failed three times to introduce 3G services in Japan. (3G services were not successfully introduced until after the acquisition by Softbank, and after conversion of Vodafone KK to Softbank-Mobile).

mobile phone handsets were inferior to the handsets offered by competitors NTT-DoCoMo and KDDI, and TuKa

and many more

Vodafone Japan? Why did it fail and sell to SoftBank? – Detailed answer

Find a long answer in this blog post below, in our other blog posts, and in some detail including statistics and financial data in our Softbank Report.

On Friday March 17, 2006, Vodafone and Softbank announced that Vodafone sells Vodafone KK (the totality of all Vodafone operations in Japan) to Softbank.

It has been reported that on Monday March 20, 2006, Softbank started to move all Vodafone KK staff, furniture and equipment from Vodafone KK’s former headquarters in the top floors of the Atago-Greenhills-Mori-Tower to Softbank headquarters in Shiodome (near Shinbashi). Also Softbank arranged very quickly that essentially all foreign expatriate managers left Vodafone KK – some stayed in Japan working for other IT companies, some returned to European Vodafone divisions, and some pursued telecom careers in USA, India, Bangladesh, or elsewhere.

By total coincidence, I had dinner with a high-level manager of Vodafone KK, of European nationality, at the indian restaurant Moti’s in Tokyo-Roppongi on exactly the same day, the Friday March 17, 2006 a few hours after the sale of Vodafone KK to Softbank was announced.

I asked him: “Which of the following is true:”

Vodafone never did any market research in Japan?

Vodafone did market research in Japan, but the quality was low?

Vodafone did market research in Japan, but nobody read it?

This Vodafone KK (Vodafone Japan) manager’s answer at the indian dinner was (3): market research was done about Japan’s mobile phone market, but the market research was not sufficiently taken into account in the business and strategy planning.

Fact is, that Vodafone KK (Vodafone Japan) took many major strategy and market decisions in Japan, which were not related to the realities of Japan’s market. Here one example. When “rebranding” (=changing the company / product / services names) from J-Phone to Vodafone, this “rebranding” campaign was centered on global roaming, i.e. Vodafone enabled Japanese customers to use Japanese J-Phone/Vodafone mobile phones in a very large number of countries outside Japan as well as inside Japan. This was at a time, when Japan’s mainstream mobile 2G phone system which both DoCoMo and J-Phone used was PDC, while much of the rest of the world, especially Europe used GSM. However, what Vodafone overlooked was, that at that time DoCoMo had about 30,000 roaming customers, out of approx. 50 million subscribers, i.e. only about 0.1% of Japanese mobile phone users used international roaming at that time. Thus Vodafone KK in Japan focused their main nation-wide poster and TV and other media campaign on about 0.1% of the Japanese market (and about 0.02% of Vodafone KK’s accessible market, given Vodafone KK’s approx. 20% market share) – less than a niche. (The reason we know how many roaming customers DoCoMo had at that time, is because one of Vodafone KK’s competitors in Japan engaged our company Eurotechnology Japan KK to analyze Japan’s roaming market, and help our client to develop strategy to better compete with Vodafone KK’s roaming products, which were aggressively marketed, and the core of Vodafone KK’s marketing focus).

Another example was Vodafone KK’s strategic focus on Japan’s prepaid market (find detailed statistics and market shares and analysis of Japan’s prepaid market in our JCOMM report). In 2006 there were about 2.6 million prepaid mobile phone customers in Japan, i.e. about 2.7% of the market, while DoCoMo had about 45,200 prepaid subscribers, i.e. about 0.09% of DoCoMo’s subscribers were prepaid customers. Since the prepaid market in Europe (especially Italy where about 1/2 of the market is prepaid) is extremely important and highly profitable, Vodafone decided on the strategy to focus strongly on the development and growth of Japan’s prepaid market. Almost at the same time however, a national campaign started in Japan linking unregistered and illegally traded prepaid mobile phones to crime, and a law was proposed in Japan’s parliament to outlaw any type of prepaid mobile phones. Thus Vodafone KK found itself on the one hand promoting and investing to develop prepaid mobile phone services in Japan, developing, purchasing (as was the business model in Japan at that time) and bringing to market special prepaid handsets, and organizing national media campaigns promoting Vodafone prepaid mobile phones, while at the same time on the other hand facing the possibility that Japan’s parliament would outlaw these same prepaid mobile phones, and a broad press and TV national discussion on how prepaid mobile phones are linked to crime. The end result was, that instead of outlawing prepaid mobile phones, it was decided to introduce far stricter registration requirements and ID requirements for mobile phones and especially for prepaid mobile phones, and the unauthorized/unregistered sale or transfer of prepaid mobile phones in Japan was made a crime. The end effect for Vodafone of course was a commercial failure of Vodafone’s prepaid mobile phone campaign, in addition to a general decrease of ARPU (average revenue per user).

Instead of focusing on its core business in Japan, Vodafone KK focused management resources, and other resources to try to influence political decisions concerning 2.7% of the market: Japan’s minute and decreasing prepaid market.

Vodafone had many other management issues in Japan, which included recruitment and personality and retain issues of top executives, many kinds of HR issues, management issues at the retail stores, handset planning issues, branding and brand management issues, localization issues and much more.

As a consequence of these and other factors, Vodafone KK’s market share continuously decreased, subscribers moved from Vodafone KK to DoCoMo and KDDI/au, and the financial performance of Vodafone KK deteriorated, in the end convincing Vodafone that the best option was to sell Vodafone’s Japan operations and terminate business activities in Japan.

You can find further details and statistics, financial performance and market share data during this period in our Softbank report and in our JCOMM report.

NOKIA’s Japan subsidiary was founded on April 3, 1989 – almost 20 years ago. On November 27, 2008 NOKIA announced to terminate selling mobile phones to Japan’s mobile operators, effectively withdrawing from Japan (except for purchasing, R&D and VERTU).

NOKIA’s sales figures in Japan were a well kept secret until last week when several Japanese newspapers wrote that NOKIA sold 200,000 phones during FY 2007: thus NOKIA’s market share was 0.39% – after 20 years of market entry efforts.

Considering the disastrous collapse of mobile phone handset sales in Japan, NOKIA’s move to quit sales in Japan actually makes a lot of sense. Nothing prevents NOKIA from re-entering Japan again in the future.

In his presentation, Dr. Fasol will explain the essentials of Japan’s mobile phone market, why and how it is so different to Europe’s. He will also talk about some of the reasons why it is so difficult for European companies to succeed and uncover opportunities and the keys to success for European companies in this important market.